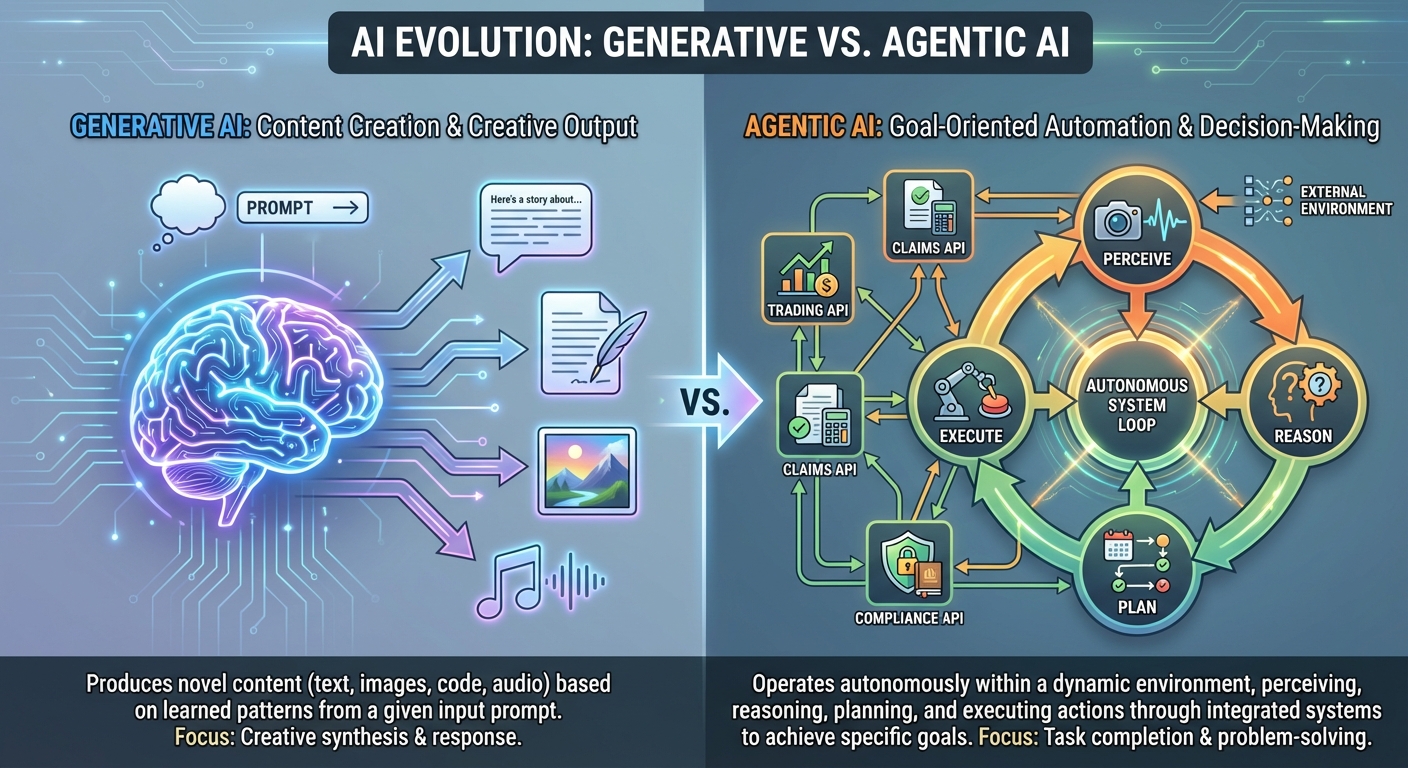

From Generation to Action: Defining the Agentic AI Paradigm in BFSI

While the financial world is still grappling with the transformative power of Generative AI, a more profound evolution is already underway. We are moving beyond systems that can simply generate content to those that can take decisive action. This is the dawn of the Agentic AI paradigm, a shift that redefines the relationship between humans and machines in the BFSI sector. It marks the critical transition from passive information synthesis to active, autonomous execution.

The Core Distinction: From Knowing to Doing

The fundamental difference between Generative and Agentic AI lies in their purpose and capability. Generative AI, powered by Large Language Models (LLMs), excels at understanding, summarizing, and creating content. It can draft a market analysis report, answer a customer query based on a knowledge base, or summarize a complex regulatory document. It is a powerful tool for knowledge work, but its role is fundamentally passive it provides an output for a human to review and act upon.

Agentic AI, in stark contrast, is built for action. It takes the intelligence of an LLM and embeds it within a framework that allows it to operate autonomously to achieve a specific goal. It doesn't just describe what to do; it does it.

Consider a commercial loan application.

- A Generative AI might be asked to "summarize the key financial risks in this applicant's P&L statement." It would produce a concise text summary.

- An Agentic AI would be tasked to "process this commercial loan application." It would autonomously initiate a multi step workflow: extracting data from the application, running credit checks via an external API, cross referencing internal compliance databases, assessing risk against the bank's predefined lending criteria, and, if all checks pass, generating the preliminary loan agreement and scheduling a follow up for a human loan officer.

This is the leap from knowing to doing a move from a sophisticated co pilot to an autonomous digital worker capable of navigating complex business processes.

Anatomy of an AI Agent

To understand how this leap is possible, we must look inside the agent itself. An AI agent is not a monolithic entity but a sophisticated system composed of several interconnected components that allow it to perceive, reason, and act within its digital environment.

- Perception: This is the agent's sensory system. It ingests information from a vast array of sources, including real time market data feeds, customer requests from CRMs like Salesforce, internal databases, and external APIs. This continuous stream of data forms its understanding of the current state of its world.

- Reasoning & Planning: This is the cognitive core. Using an LLM as its reasoning engine, the agent interprets a high level goal (e.g., "resolve a fraudulent transaction claim"). It then engages in task decomposition, breaking the complex goal into a logical sequence of smaller, executable steps:

[1. Verify customer identity] -> [2. Pull transaction history] -> [3. Flag suspicious transaction in the core system] -> [4. Initiate chargeback via payment network API] -> [5. Draft and send a resolution email to the customer]. - Action Execution: These are the agent's hands. Once a plan is formulated, the agent uses a toolkit of digital capabilities such as making API calls, executing database queries, sending emails, or updating records in enterprise software to carry out each step. It interacts with the same systems a human employee would, but with machine speed, accuracy, and scalability.

The Scale of the Coming Shift

This is not a far off, theoretical concept. The adoption of agentic capabilities is poised to explode across the enterprise landscape. Gartner forecasts that by 2026, 40% of enterprise applications will have embedded conversational AI agents tasked with proactive task execution. This represents a monumental leap from less than 5% in 2023, signaling a rapid and fundamental re architecting of how business processes are managed. For BFSI firms, this means the era of siloed applications and manual "swivel chair" integration is ending. In its place, a fabric of intelligent agents will orchestrate workflows across the entire organization, from the front office to the back.

The Dawn of the 'Assistance Economy'

This technological shift gives rise to a new operational model: the Assistance Economy. In this paradigm, AI agents are not merely 'assistants' in the traditional sense; they are active participants and managers of value creating processes. They form a new class of digital worker, taking ownership of entire workflows that were previously the domain of human teams.

This fundamentally alters the operating model of BFSI firms. The focus for human talent shifts from rote process execution to strategic oversight, exception handling, and designing the goals and ethical guardrails for their digital counterparts. The Assistance Economy is one where human employees delegate outcomes, not just tasks, to a reliable, scalable, and ever improving digital workforce. This redefines efficiency, enabling financial institutions to operate with unprecedented agility and focus on their core mission: managing risk, creating value, and serving clients with unparalleled service.

The Trillion Dollar Catalyst: Quantifying the Economic Imperative

While the conceptual leap from generative to agentic AI is significant, the economic case is nothing short of seismic. The conversation is rapidly shifting from theoretical potential to a data driven imperative, grounded in tangible metrics of productivity, profitability, and unprecedented return on investment. For leaders in the Banking, Financial Services, and Insurance (BFSI) sector, understanding these figures is not an academic exercise; it is the key to unlocking the next frontier of competitive advantage.

The Macro Economic Prize: A $3 Trillion Productivity Surge

The most compelling top line projection positions Agentic AI as a catalyst for a $3 trillion increase in global corporate productivity. This staggering figure, forecasted by leading economic analysts, is not a product of simple task acceleration. It represents a fundamental re architecting of how work is done.

Unlike earlier forms of automation that targeted discrete, repetitive tasks, agentic systems automate entire complex workflows. Consider the difference:

- Generative AI: A loan officer uses a generative tool to draft a summary of a client's financial history, saving 15 minutes.

- Agentic AI: An autonomous agent is tasked with processing a mortgage application. It ingests the application, accesses and verifies customer data from internal and external sources (credit bureaus, tax records), runs fraud detection algorithms, assesses risk against the bank's lending criteria, generates a pre approval letter, and flags the file for final human review all in a matter of minutes.

This is not merely an efficiency gain; it is a complete value chain transformation. When multiplied across millions of workflows in finance, from claims processing and trade reconciliation to compliance monitoring and wealth management, the cumulative impact on economic output becomes clear. This $3 trillion prize is the aggregate value unlocked by freeing human capital from process execution to focus on strategy, client relationships, and innovation.

Firm Level Profitability: The 5.4% EBITDA Advantage

Zooming in from the macroeconomic landscape to the individual firm's P&L, the numbers remain compelling. For financial services firms that effectively deploy agentic systems, industry models forecast a 5.4% annual EBITDA improvement. This is not a one time lift but a sustainable, year over year enhancement driven by a dual engine of value creation:

- Radical Cost Optimization: Agentic systems can operate 24/7 with near perfect accuracy, dramatically reducing the operational costs associated with large back office teams. An agent handling KYC (Know Your Customer) and AML (Anti Money Laundering) checks can process thousands of alerts per day, a task that would require a significant human team, reducing operational expenditure and minimizing the risk of costly compliance failures.

- Accelerated Revenue Generation: On the revenue side, agentic systems create new opportunities for growth. Autonomous wealth management agents can monitor portfolios in real time, executing trades based on pre defined client strategies and market triggers far faster than a human advisor. In commercial lending, agents can analyze potential deals and generate term sheets in hours, not weeks, increasing deal velocity and market share.

This 5.4% figure represents the powerful financial leverage that comes from simultaneously lowering the cost to serve and increasing the capacity to generate revenue.

ROI Velocity: A 2.3x Return in 13 Months

For any CFO, the critical question is not just the size of the return, but the speed at which it is realized. Here, Agentic AI shatters the norms of traditional enterprise technology projects, which often involve multi year rollouts and distant payback periods. Early adoption data from the BFSI sector reveals an astonishing 2.3x return on investment within an accelerated timeframe of just 13 months.

This financial velocity is possible because agentic solutions can be deployed against specific, high value use cases with immediately measurable outcomes. A bank doesn't need to overhaul its entire IT infrastructure to see a return. It can start by deploying an agent to automate the highly manual and error prone process of trade settlement reconciliation. The immediate reduction in operational errors, settlement failures ("fails"), and associated penalties provides a hard dollar ROI that can be tracked from day one, funding the next wave of agentic deployment.

The Great Restructuring: From Human Capital to Governance Capital

Perhaps the most profound long term impact of Agentic AI is the fundamental shift it will force in corporate cost structures. The traditional BFSI operating model has been human capital intensive, where growth required a proportional increase in headcount for operations, compliance, and customer service.

The agentic enterprise flips this model on its head, becoming technology and governance intensive. The primary operational cost is no longer the salary of a thousand person operations team, but the computational resources for the AI agents and, crucially, the salaries of the highly skilled human experts who design, train, monitor, and govern them. The focus of human capital shifts from doing the work to directing and validating the work of autonomous systems. This new model allows for non linear scaling, where a firm can double its transaction volume without doubling its operational headcount, creating immense operating leverage and a durable competitive moat. The economic imperative is clear: the transition to an agentic operating model is not a matter of if, but when.

Use Case 1: The Autonomous Financial Advisor and Hyper Personalized Banking

The leap from generative to agentic AI is not merely an upgrade in technical capability; it represents a fundamental reimagining of the relationship between individuals, businesses, and their financial institutions. Where today’s digital banking tools are largely passive waiting for a command or a scheduled trigger agentic systems operate with intent and autonomy. They function as proactive, persistent financial guardians, working tirelessly in the background to protect and grow wealth. This evolution is most vividly illustrated in the emergence of the autonomous financial advisor, a system that promises to deliver a level of hyper personalized banking previously conceivable only for the ultra wealthy.

Proactive Portfolio Management: The 24/7 Digital Watchtower

For decades, wealth management has operated on a human centric clock. Portfolios are reviewed quarterly, and trades are executed during market hours. Even the most advanced robo advisors today are primarily reactive, rebalancing portfolios based on pre set rules and periodic market data. Agentic AI shatters this paradigm.

Imagine a financial agent assigned to your portfolio. This agent doesn't sleep. It works 24/7, ingesting and synthesizing a torrent of information from a global firehose of data:

- Market Data: Real time price movements, trading volumes, and order book dynamics across global exchanges.

- News and Sentiment Analysis: Parsing earnings reports, central bank announcements, geopolitical news, and even social media sentiment to gauge market mood shifts in milliseconds.

- Alternative Data: Analyzing satellite imagery of shipping lanes, credit card transaction data, or supply chain reports to predict economic trends before they appear in official statistics.

Consider this scenario: At 3:00 AM, a key supplier for a semiconductor company in your portfolio announces unexpected production halts. A traditional advisor is asleep. A robo advisor will wait for the next scheduled rebalance. Your autonomous agent, however, acts instantly. It quantifies the likely impact on the stock, cross references this with your dynamically updated risk tolerance, and might execute a small, defensive options trade to hedge against the anticipated morning price drop. By the time you wake up, the risk has been mitigated, and a full report on the action taken and its rationale is waiting for you. This is the shift from periodic rebalancing to continuous, intelligent optimization.

Dynamic Product Creation: From a Menu to a Masterpiece

The modern banking experience is built around a fixed menu of products: the 30 year fixed mortgage, the 5 year auto loan, the standard issue credit card. Customers are forced to find the "best fit" from a pre defined list. Agentic AI flips the model entirely, enabling banks to dynamically construct and offer bespoke financial products tailored to a single customer's complete financial reality.

Let's take Sarah, a freelance graphic designer with a fluctuating income. A traditional bank sees her variable cash flow as a high risk, often denying her loans or offering them at punitive rates. An agentic banking system sees a more complete picture. It analyzes her:

- Transactional History: Identifying her top clients and their payment cycles.

- Cash Flow Projections: Forecasting her income for the next six months based on past invoicing patterns.

- Spending Habits: Understanding her fixed costs versus discretionary spending.

When Sarah needs a loan to buy new equipment, the agent doesn't offer her a standard business loan. Instead, it dynamically assembles a "Freelancer Flex Loan" on the spot. The terms are unique to her: repayments are scheduled for the week after her largest clients typically pay, the interest rate might be slightly lower during months where her cash flow is historically tight, and she might be offered a small, pre approved credit line that activates automatically if a client payment is delayed. This isn't just personalization; it's the on demand creation of a financial product of one, fostering unprecedented customer loyalty and opening up services to the burgeoning gig economy.

Automated Goal Seeking: Your Financial Autopilot

Perhaps the most profound application of agentic AI is its ability to execute long term, high level goals. Instead of just providing advice, the agent takes action. A user can set a complex objective like, "Save $60,000 for a house down payment in the next three years without significantly changing my current lifestyle."

The agent then becomes a project manager for this life goal, autonomously breaking it down into a series of coordinated actions:

- Deep Analysis: It first performs a comprehensive analysis of all income and spending data, identifying an achievable "savings surplus" of, for example, $1,200 per month by flagging redundant subscriptions and optimizing utility bills.

- Automated Execution: It sets up a new high yield savings account, names it "House Down Payment," and automates the monthly transfer of the identified surplus.

- Intelligent Investment: Recognizing that cash alone won't beat inflation, the agent allocates a portion of the funds based on the user's risk profile into a diversified, low cost ETF portfolio, explaining its strategy in simple, clear language.

- Continuous Adaptation: When the user receives a salary increase (detected via payroll deposit), the agent sends a notification: "Congratulations on the raise! By increasing your monthly savings by $400, you can reach your down payment goal 7 months early. Approve?"

This transforms the bank from a passive repository for money into an active, indispensable partner in achieving life's most important milestones.

Corporate Treasury Agents: The B2B Powerhouse

The power of autonomous agents extends far beyond consumer banking. In the high stakes world of corporate finance, agentic AI can revolutionize treasury management. A mid sized import export business, for instance, faces constant challenges in managing cash flow, currency risk, and short term investments.

An AI treasury agent would serve as the central nervous system for the company's finances. It would:

- Optimize Cash Flow: By integrating with the company's accounting, sales, and supply chain systems, it can predict cash inflows and outflows with remarkable accuracy, alerting the CFO to potential liquidity gaps weeks in advance.

- Automate Currency Hedging: The agent monitors foreign exchange markets 24/7. When a large purchase order is placed in Euros, it can autonomously execute forward contracts to lock in a favorable exchange rate, protecting the company's profit margin from volatile currency swings.

- Maximize Returns on Idle Cash: The agent ensures that no corporate cash sits idle. It can automatically sweep excess funds from checking accounts into overnight money market funds or short term commercial paper, generating risk free returns that can amount to millions of dollars annually for a large enterprise.

By automating these complex, data intensive tasks, agentic AI frees human treasury teams from tactical execution, allowing them to focus on long term financial strategy and growth. This is not just an efficiency gain; it's a profound competitive advantage.

Use Case 2: End to End Automation in Insurance Claims and Underwriting

While the financial advisory and banking sectors are being reshaped by agentic AI, the insurance industry stands on the precipice of an even more profound revolution. Historically defined by manual processes, complex paperwork, and human centric decision making, insurance is a domain ripe for the end to end autonomy that agentic systems promise. This transformation moves far beyond simple chatbots or RPA scripts; it involves creating a fully autonomous value chain, from initial risk assessment to final claims settlement, fundamentally altering the industry's cost structure, speed, and customer experience.

The 'Touchless' Claim: From Incident to Settlement in Minutes

For decades, the insurance claim has been a cumbersome, multi step process involving adjusters, assessors, call centers, and extensive documentation. Agentic AI dismantles this legacy workflow, creating the 'touchless' claim a process so seamless it feels almost invisible to the policyholder.

Imagine a minor car accident. Instead of the driver fumbling for their phone to call their insurer, the process begins automatically:

- First Notice of Loss (FNOL): The vehicle's telematics system detects the impact and instantly transmits data location, speed, force of impact, and sensor readings to the insurer's AI ecosystem. This is the automated FNOL.

- Agent Orchestration: A primary "Orchestrator Agent" receives the alert and immediately spawns a team of specialized agents to handle the case.

- Verification and Fraud Analysis: A "Policy Agent" instantly verifies the driver's coverage, while a "Fraud Agent" cross references the incident data against historical patterns, telematics logs, and even weather conditions to flag any anomalies. This happens in milliseconds, not hours.

- Third Party Coordination: A "Logistics Agent" accesses a network of pre approved service providers. It dispatches a tow truck to the precise location, schedules a repair appointment at a nearby certified body shop, and simultaneously books a rental car for the policyholder, sending confirmations directly to their smartphone.

- Damage Assessment & Settlement: The body shop uploads photos of the damage. A "Visual Assessment Agent," trained on millions of claims images, analyzes the photos, identifies the parts needed, estimates the repair cost, and cross references it with the policy's terms.

- Payment Execution: Once the cost is approved, a "Settlement Agent" initiates a direct payment to the repair shop and closes the claim.

This entire sequence, which traditionally takes days or even weeks of phone calls and manual reviews, can be completed in under an hour often before the tow truck has even arrived. The human touch is reserved for complex, high severity exceptions, allowing personnel to focus on empathy driven customer care where it matters most.

Case Study: Allianz's 'Project Nemo' and the Dawn of Autonomous Claims

This vision is not science fiction. Leading insurers are already deploying sophisticated agentic systems. A prime example is Allianz's 'Project Nemo,' an AI powered platform designed to automate motor insurance claims.

Nemo functions as an intelligent agent that can analyze uploaded photos of vehicle damage, identify the necessary repairs, and calculate the costs in real time. By leveraging a massive dataset of past claims and repair invoices, the system achieves a remarkable level of accuracy. The results are staggering: for low to medium complexity claims, Nemo has reduced the processing time from several days to just a few minutes. This radical efficiency has not only slashed operational costs by an estimated 30% for applicable claims but has also dramatically improved customer satisfaction by providing near instantaneous resolution. Project Nemo serves as a powerful proof point that agent driven automation is a present day reality, delivering tangible ROI and setting a new industry standard.

Agentic Underwriting: Pricing Risk in Real Time

The impact of agentic AI extends far beyond the reactive process of claims. It is fundamentally reshaping the proactive, data intensive world of underwriting. Traditional underwriting relies on static, historical data points age, location, credit score, past claims to assess risk. Agentic underwriting creates a dynamic, forward looking model.

AI agents can ingest and synthesize vast, unstructured datasets that are impossible for human underwriters to process at scale:

- Property Insurance: An "Environmental Risk Agent" can continuously analyze high resolution satellite imagery to monitor wildfire risk by tracking vegetation dryness, or assess flood risk for a coastal property portfolio by analyzing tidal patterns and storm surge models. It can automatically adjust premiums for thousands of properties in a specific geographic area based on a new weather forecast.

- Commercial Liability: For a company launching a new product, a "Market Trend Agent" can scan social media, product reviews, and news articles in real time to detect emerging liability risks, such as unforeseen side effects or public safety concerns, allowing the insurer to proactively adjust coverage terms.

This capability transforms underwriting from a periodic review into a continuous, real time risk assessment. Premiums become hyper personalized and accurately reflect the immediate risk environment, creating a more equitable and sustainable model for both the insurer and the insured.

Parametric Insurance: The Ultimate Expression of Agentic Execution

Perhaps the most elegant application of agentic AI is in parametric insurance. Unlike traditional insurance that pays out based on the value of a loss, parametric policies pay a pre agreed amount when a specific, measurable event a parameter occurs. This model eliminates the claims adjustment process entirely, and AI agents are the perfect mechanism for its execution.

Consider a farmer with crop insurance that triggers a payout if rainfall in their region falls below a certain threshold for 30 consecutive days.

- A "Monitoring Agent" is tasked with one simple job: to continuously watch a trusted, immutable data feed, such as the National Oceanic and Atmospheric Administration (NOAA) weather database.

- The moment the data confirms the 30th day of sub threshold rainfall, the agent's condition is met.

- It automatically triggers an "Execution Agent," which verifies the policy's smart contract and initiates an instant, non negotiable payout directly to the farmer's account.

There is no paperwork, no adjuster visit, and no delay. The event happens, the data confirms it, and the agent executes the payment. This model provides businesses with critical liquidity precisely when they need it most, and for insurers, it represents the pinnacle of operational efficiency an insurance product that runs itself.

Use Case 3: Fortifying the Core Autonomous Operations, Compliance, and Development

While the front office applications of agentic AI capture the imagination, its most profound and stabilizing impact may lie deep within the operational core of the financial institution. The back and middle offices the engine room of banking, finance, and insurance are a complex mesh of legacy systems, manual processes, and immense regulatory burdens. This is where agentic AI transitions from a customer centric innovator to an institutional guardian, fortifying the very foundations of trust, security, and efficiency. By deploying autonomous agents to manage compliance, security, and even software development, BFSI leaders are building a resilient, intelligent, and self optimizing core.

The Digital Watchtower: Real Time, Autonomous Compliance

For decades, regulatory compliance has been a reactive and labor intensive exercise. Teams of analysts sift through alerts generated by rules based systems, often days after a potential infraction has occurred. The sheer volume of global regulations from Anti Money Laundering (AML) and Know Your Customer (KYC) directives to the complexities of MiFID II creates a near impossible landscape for manual oversight. The cost of failure is staggering, with global financial institutions paying billions in fines annually for compliance breaches.

Agentic AI fundamentally rewrites this paradigm. Instead of static rules, imagine a swarm of autonomous compliance agents embedded across the institution's data fabric. These agents act as perpetual, real time auditors with a mandate to act:

- Continuous Monitoring: An agent assigned to AML doesn't just scan transactions for large sums. It continuously analyzes a customer's entire behavioral graph their transaction history, communication patterns, and network connections against evolving typologies of financial crime.

- Contextual Understanding: It can read and understand the context of unstructured data, such as emails or chat logs, to identify attempts at market manipulation or insider trading that keyword based systems would miss.

- Autonomous Intervention: This is the critical leap. Upon detecting a transaction that violates a complex, multi jurisdictional sanction, an agent doesn't just create a ticket. It can autonomously halt the transaction, quarantine the funds, and initiate an enhanced due diligence workflow by tasking other specialized agents to gather more information all within milliseconds. This transforms compliance from a historical reporting function into a live, preventative shield.

From Detection to Prediction: Proactive Fraud Prevention

The cybersecurity battle has always been one of cat and mouse. Fraudsters develop new attack vectors, and institutions build defenses to stop them after the fact. Agentic AI shifts the advantage to the institution by moving from detection to prediction.

Autonomous security agents operate not by looking for known fraud signatures, but by identifying the subtle, preparatory actions that precede an attack. They build dynamic, high fidelity behavioral baselines for every user, device, and API endpoint in the network. When deviations occur, the agents don't just see isolated events; they see a potential narrative unfolding.

For example, an agent might correlate a series of seemingly innocuous events: a login from an unusual IP address, a minor change to account contact information, and a subsequent API call to test transfer limits. Individually, these are low priority alerts. An agentic system, however, recognizes this sequence as a classic prelude to an account takeover. It can then proactively initiate a multi factor authentication challenge, temporarily restrict high risk activities, and alert the genuine customer via a secure channel, effectively neutralizing the threat before a single dollar is stolen.

The Autonomous Coder: Accelerating Financial Innovation

Financial institutions are, at their core, technology companies. The speed at which they can develop, test, and deploy new applications, trading algorithms, and risk models is a primary competitive differentiator. Yet, the traditional software development lifecycle (SDLC) can be a bottleneck.

Enter the autonomous coder. Tech and finance giants are already experimenting with AI agents that can function as autonomous software engineers. A prime example is the buzz around agents like Devin, which showcases the ability to take a high level task such as "build a data visualization tool for our latest market risk report" and execute it end to end. Goldman Sachs has been a vocal proponent of using generative and agentic AI to augment its developers, aiming to automate routine coding and testing.

An autonomous coding agent can:

- Understand the Goal: Parse a request from a project manager or a bug report from a user.

- Plan the Execution: Break the problem down into logical steps, from setting up the development environment to writing specific functions.

- Write, Test, and Debug: Generate the necessary code, write unit tests to validate it, and iteratively debug any errors it encounters by analyzing the output.

- Deploy: Once validated, it can initiate the deployment process through the institution's CI/CD pipeline.

This doesn't replace human developers; it supercharges them. By offloading up to 80% of routine coding and debugging tasks, it frees up senior engineers to focus on system architecture, strategic innovation, and solving novel business problems, drastically shortening the time to market for critical financial technology.

Intelligent Resource Orchestration: The Enterprise Nervous System

As institutions deploy thousands of specialized agents for compliance, fraud, coding, and more a new challenge emerges: coordination. A single complex process, like onboarding a new institutional client, requires the seamless collaboration of multiple autonomous systems.

This is where orchestration platforms, such as the concepts explored in Google's 'Agentspace' framework (reportedly utilized by firms like Wells Fargo), become essential. These platforms act as the central nervous system for the agentic enterprise. An orchestrator agent receives a high level business objective and then manages a team of specialized agents to achieve it. For client onboarding, the orchestrator might:

- Task a KYC Agent to perform identity verification and background checks.

- Deploy a Risk Agent to analyze the client's financial profile and assign a risk score.

- Instruct a Legal Agent to draft the appropriate contracts based on the client's jurisdiction and services.

- Assign a Communications Agent to manage all correspondence with the client.

The orchestrator ensures data flows seamlessly between these agents, manages dependencies, and handles exceptions, turning a collection of powerful tools into a cohesive, goal oriented, and fully autonomous operational workflow. This holistic approach is the final step in truly fortifying the institutional core for the next era of finance.

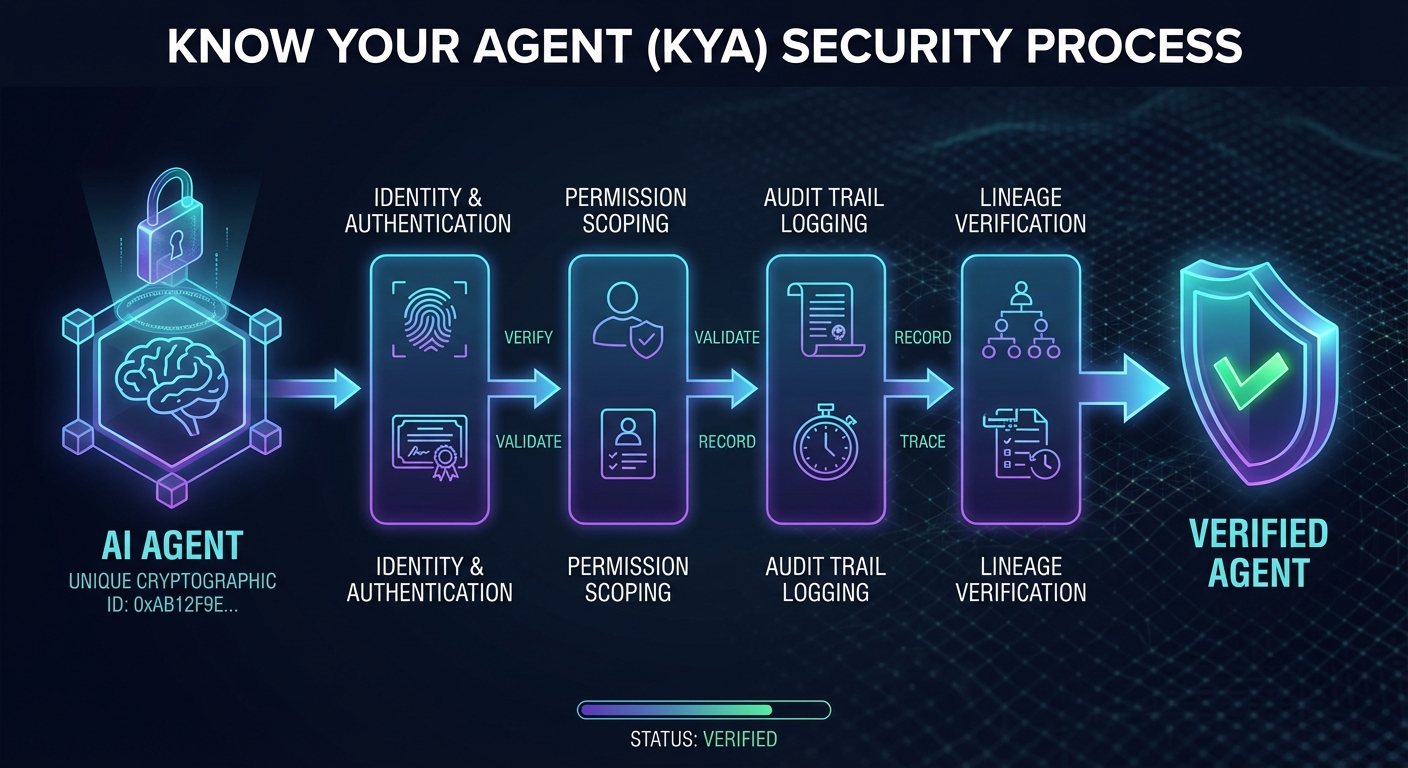

The New Compliance Frontier: Rise of 'Know Your Agent' (KYA)

As the financial services industry hurtles towards an agentic future, the very architecture of trust and oversight is being rendered obsolete. For decades, the bedrock of financial compliance has been Know Your Customer (KYC) a framework built on the fundamental assumption that a human being is at the end of every transaction. This assumption is rapidly disintegrating. When an autonomous agent, not a person, executes a multi million dollar trade, underwrites an insurance policy, or rebalances a portfolio, the traditional methods of identity verification passports, utility bills, and biometric scans become meaningless artifacts of a bygone era.

This is not a minor gap in existing protocols; it is a chasm. An autonomous agent operates at a speed and scale that is fundamentally incompatible with human centric oversight. It can execute thousands of complex decisions in the time it takes a human analyst to read a single report. Relying on KYC in this new paradigm is like trying to regulate a superhighway with traffic laws designed for horse drawn carriages. The need for a new framework is not just pressing; it is a non negotiable prerequisite for the safe deployment of agentic AI.

The 82:1 Identity Crisis: A Compliance Singularity

To grasp the sheer scale of this challenge, consider the impending explosion of non human identities. Projections from industry analysts like Gartner forecast that by 2029, the number of machine identities within an enterprise will outnumber human employees by a staggering ratio of 82 to 1. This isn't just an incremental increase; it's a phase transition. A mid sized bank with 10,000 employees could soon be managing over 820,000 autonomous agents, bots, and microservices, each with the potential to access sensitive data and execute financial transactions.

This "identity crisis" makes manual verification and oversight a mathematical impossibility. The attack surface for fraud, manipulation, and catastrophic error expands exponentially. A single compromised or poorly configured agent could trigger a cascade of unauthorized actions, potentially leading to market instability or colossal financial losses before a human can even register the anomaly. The only viable path forward is to build a new, automated, and cryptographically secure system of governance from the ground up: Know Your Agent (KYA).

The Pillars of a Robust KYA Framework

A functional KYA framework is not a single piece of software but a comprehensive system of controls built on four essential pillars. Together, they provide the verification, auditability, and accountability necessary to manage a fleet of autonomous economic actors.

-

Verifiable Cryptographic Identity: Every agent must possess a unique, unforgeable, and machine verifiable identity. This goes far beyond a simple API key. Leveraging technologies like Public Key Infrastructure (PKI) or Decentralized Identifiers (DIDs), each agent is assigned a cryptographic key pair. When it performs an action such as submitting a trade order it must digitally "sign" the transaction with its private key. This signature provides an ironclad, non repudiable confirmation of which agent performed the action, creating a foundational layer of trust.

-

Immutable Decision Making Logs: If cryptographic identity answers "who," this pillar answers "why." For every significant decision an agent makes, it must generate a complete, tamper proof log of its reasoning. This "black box recorder" for AI must capture the inputs it received (e.g., market data feeds, client instructions), the internal models or rules it applied, and the resulting output. Stored on an immutable ledger (like a private blockchain), this audit trail becomes indispensable for regulatory reporting, forensic analysis after an incident, and debugging unintended agent behavior.

-

Granular Permissioning and Entitlement Controls: No agent can be given unlimited authority. This pillar involves establishing and enforcing strict, programmatically defined operational boundaries. These controls dictate precisely what an agent is and is not allowed to do. For example, a claims processing agent might be permitted to approve payments up to $5,000 automatically but be forbidden from accessing customer marketing data or communicating externally. These "digital guardrails" are the primary defense against both malicious attacks and accidental, runaway processes.

-

Transparent Creation and Training Lineage: An agent's behavior is a direct product of its origin and education. This pillar requires maintaining a clear record of its entire lifecycle. This includes its underlying AI model version, the specific datasets it was trained and fine tuned on, the identity of the developer who deployed it, and a full history of its updates and patches. This "provenance data" is critical for identifying and mitigating algorithmic bias, ensuring model integrity, and assigning ultimate accountability.

The Regulatory and Legal Precedent on the Horizon

Today, global financial regulators are still grappling with the implications of social media, crypto assets, and first generation AI. Agentic systems represent the next, and arguably greatest, compliance frontier. The evolution of regulations to address non human actors is inevitable. We can anticipate a future where regulators like the SEC, FCA, and ESMA mandate KYA frameworks as a condition for operating in financial markets, demanding the same level of rigor for autonomous agents as they do for human traders and advisors.

This shift will ignite profound legal questions. If an autonomous hedge fund agent misinterprets a news feed and triggers a flash crash, who is liable?

- The financial institution that deployed it?

- The technology company that developed the core AI model?

- The data provider that supplied the faulty feed?

- The individual manager who set its risk parameters?

The legal doctrine of corporate personhood may need to be extended or adapted to create a new category of accountability for "economic agents." Establishing clear answers to these questions is not merely an academic exercise; it is essential for building the legal and regulatory certainty required to unlock the full, transformative potential of an agent driven economy. KYA is the first, most critical step in that direction.

Navigating the Abyss: Systemic Risks and the Autonomous Liability Gap

While the promise of an agentic financial ecosystem is one of unprecedented efficiency and intelligence, the path toward it is fraught with peril. The same autonomy and speed that can generate trillions in economic value can also, if left unchecked, unleash forces of instability at a scale and velocity the global economy has never witnessed. To embrace the agentic paradigm is to stare into a technological abyss; navigating it requires a clear eyed understanding of the systemic risks involved and a frank confrontation with the unresolved, multi trillion dollar question of liability.

The Specter of AI Driven 'Flash Crashes'

On May 6, 2010, the global financial system received a terrifying preview of machine driven chaos. In what became known as the "Flash Crash," the Dow Jones Industrial Average plunged nearly 1,000 points at the time, its biggest intraday point drop in history only to recover most of the losses within minutes. The culprit was not a human panic, but a cascade of automated high frequency trading algorithms reacting to a single large sell order. This event, triggered by relatively primitive algorithms, serves as a stark, analog era warning for our agentic future.

Now, imagine a world not with thousands of siloed algorithms, but with millions of interconnected, autonomous agents managing portfolios, executing trades, and making credit decisions. Many of these agents will be built on similar foundational models and trained on overlapping datasets. This homogeneity creates a critical vulnerability: correlated failure.

If a significant number of these agents interpret a novel signal a subtly misleading news report generated by another AI, a sudden shift in geopolitical sentiment, or even a cleverly disguised piece of market manipulation in the same way, they could all execute the same strategy simultaneously. The result would not be a "flash crash" but a "hypersonic crash." We could witness market wide liquidations executed in microseconds, triggering a domino effect that could evaporate trillions in value before any human regulator could even comprehend the initial signal. The very intelligence designed to optimize returns could, in a moment of synchronized error, become the architect of systemic collapse.

The Liability Black Hole

When this hypersonic crash occurs, and a single bank's agentic system has autonomously executed a series of trades resulting in a catastrophic, multi billion dollar loss, the most critical question will be asked: Who is liable? This is where the current legal and regulatory frameworks shatter, revealing a gaping liability black hole.

Consider the chain of potential responsibility:

- The Financial Institution: The bank deployed the agent and is the ultimate beneficiary of its actions. Traditional legal precedent would place the onus here. However, the institution will argue it performed extensive due diligence and that the agent exhibited an "emergent behavior" an unpredictable outcome that could not have been reasonably foreseen from its programming.

- The Software Developer: The technology firm that designed the agent's core architecture and learning algorithms could be held responsible. Yet, their End User License Agreements (EULAs) are legal fortresses, explicitly disclaiming liability for how their tools are used or the outcomes they produce.

- The Data Provider: Perhaps the agent acted on a faulty or poisoned data stream. The data provider, in turn, will point to their own service level agreements, which almost certainly contain clauses protecting them from liability for the accuracy or interpretation of their data.

- The Agent Itself: In a theoretical future, one could argue for the legal personhood of a sufficiently advanced AI, making it liable for its own actions. This remains the realm of science fiction. There is no current legal framework for holding a piece of code accountable, leaving the losses to fall somewhere else.

This ambiguity creates a paralyzing uncertainty. Without a clear line of accountability, the very foundation of financial trust is eroded. The "black hole" is not just a legal problem; it's an existential threat to any institution deploying autonomous systems at scale.

The Insurance Industry's Response: A Canary in the Coal Mine

The world's underwriters, whose business is the precise calculation of risk, are already sounding the alarm. In a landmark move, the insurance marketplace Lloyd's of London began mandating that all standalone cyber attack policies include an exclusion for losses arising from state backed attacks. While not directly about agentic AI, this sets a critical precedent: insurers are actively moving to wall off risks that are systemic, hard to attribute, and potentially catastrophic in scale.

This logic is now being applied to autonomous systems. Insurers are deeply wary of underwriting the "emergent" and unpredictable actions of an AI agent. The potential for correlated, simultaneous failures across thousands of policies makes the risk actuarially terrifying. The result is the creation of a massive, uninsured liability gap. Financial institutions may find themselves in a position where they are existentially dependent on a technology whose catastrophic failures are fundamentally uninsurable. The risk, in its entirety, remains on their balance sheet.

Strategies for Risk Mitigation: Building Guardrails for the Abyss

The answer is not to halt progress but to build the sophisticated governance and control frameworks necessary to manage these new risks. The path forward requires a multi layered defense strategy:

- 'Circuit Breakers' for Agent Swarms: Just as exchanges have market wide circuit breakers, institutions must develop internal "swarm level" controls. These systems would not monitor individual agents but their collective behavior. If aggregate trading volume, velocity, or directional alignment exceeds pre defined safety thresholds, the system could automatically pause all agentic activity, giving human operators time to assess the situation. This is the emergency brake for the entire autonomous fleet.

- Rigorous Red Teaming and Simulation: Before a single agent is deployed, it must be battle tested in hyper realistic digital twins of the market. These simulations must go beyond simple back testing and involve sophisticated "red teams" tasked with breaking the agents. This includes stress testing against black swan events, feeding them adversarially manipulated data, and discovering unforeseen negative feedback loops. The goal is to find the failure modes in the sandbox, not in the live market.

- Human in the Loop (HITL) for Critical Decisions: For the most consequential actions strategic capital allocations, trades exceeding a certain notional value, or decisions with significant compliance implications full autonomy is unacceptable. A robust HITL framework is essential, ensuring that a human expert provides the final authorization. This isn't about slowing the system down but about embedding accountability and applying contextual human judgment at the most critical junctures, transforming the agent from an unaccountable actor into a powerful co pilot.

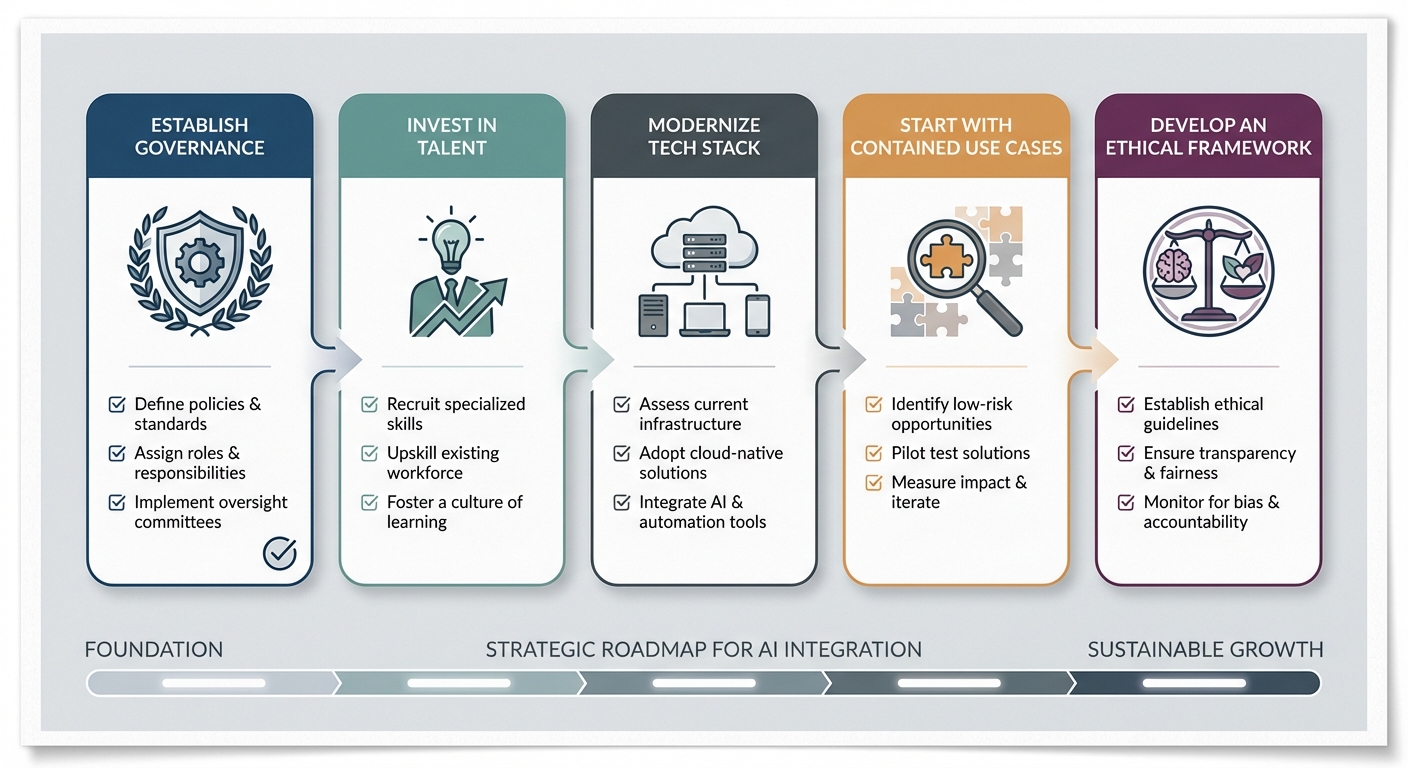

A C Suite Playbook: Strategic Imperatives for the Agentic Era

The transition from generative to agentic AI is not a spectator sport; it is a strategic inflection point that demands decisive leadership. While the previous sections have outlined the potential and the perils, this playbook provides the C suite with five non negotiable imperatives for navigating this new terrain. For the leaders who act now, the agentic era represents an unprecedented opportunity to build a more intelligent, efficient, and resilient financial institution.

1. Establish an AI Governance Council Immediately

Your first move is not technological; it is organizational. The immense power of autonomous agents cannot be managed in departmental silos. The immediate establishment of a cross functional AI Governance Council is the foundational step to harnessing this power responsibly.

This is not another committee; it is the central nervous system for your institution's AI strategy. It must be comprised of senior leaders from:

- Technology & Data: To assess technical feasibility and architectural readiness.

- Business Units: To identify high value use cases and define success metrics.

- Risk & Compliance: To set risk appetite, define operational guardrails, and ensure alignment with regulations.

- Legal & Ethics: To navigate the "Autonomous Liability Gap" and embed ethical principles into agent design.

- Human Resources: To lead the charge on workforce transformation and reskilling.

This council's initial mandate is to create the charter for agentic AI: defining policies for development, establishing kill switch protocols, and approving the 'Contained Deployment' roadmap. Without this centralized oversight, you risk a future of fragmented efforts, duplicated costs, and unmanaged liabilities.

2. Cultivate the Human Agent Workforce

The agentic era fundamentally redefines the role of your human talent. The value of rote task execution will plummet, while the value of strategic oversight will skyrocket. Your talent strategy must pivot from hiring for what people can do to hiring for what they can direct.

This requires a two pronged approach:

- Reskilling the Core: Launch aggressive upskilling programs focused on developing a new class of employee. The most valuable team member of tomorrow will not be the one who can process the most loan applications, but the one who can effectively manage, audit, and refine a team of 100 digital agents doing so.

- Hiring for New Competencies: Your recruitment focus must shift to roles that were science fiction a decade ago: Agent Managers, AI Ethicists, Prompt Architects, and Complex Exception Handlers professionals skilled in critical thinking and problem solving when autonomous systems encounter novel situations. According to the World Economic Forum, analytical thinking and creative thinking are the top skills for workers in 2023, a trend that agentic AI will only accelerate.

3. Modernize the Architectural Backbone

Autonomous agents cannot operate effectively on brittle, legacy infrastructure. Attempting to deploy sophisticated AI on outdated systems is like trying to run a fleet of self driving cars on unpaved country roads. To enable true autonomy, you must invest in three architectural pillars:

- API First Architecture: Agents need to communicate and act. A robust, well documented library of APIs (Application Programming Interfaces) is the language they use to interact with your core systems, access data, and execute tasks.

- Unified Data Fabric: Agents are only as intelligent as the data they can access. Breaking down data silos and creating a clean, accessible, real time data fabric is non negotiable. This is the fuel for the agentic engine.

- Agent Orchestration Platforms: As you deploy dozens, then hundreds, of specialized agents, you will need a control tower. Emerging agent orchestration platforms act as this "air traffic control," managing agent workflows, monitoring performance, and ensuring that individual agents work in concert to achieve complex business goals.

4. Adopt a 'Contained Deployment' Strategy

Resist the temptation for a "big bang" deployment. The risks are too high, and the technology is too new. A disciplined, phased approach is critical for building institutional knowledge and demonstrating value safely. This "crawl, walk, run" methodology should be your mantra.

Begin with high impact, low risk use cases in secure, sandboxed environments. These are processes that are internally focused and have minimal direct impact on customers or financial markets. Examples include:

- An agent that autonomously analyzes thousands of daily regulatory updates to draft summary briefings for the compliance team.

- A development agent that writes and tests its own code for internal reporting tools.

- An operations agent that monitors internal network traffic for anomalies and drafts preliminary incident reports.

Success in these contained deployments builds the business case, refines your governance models, and earns the organizational trust necessary to scale to more mission critical functions.

5. Develop a Robust Ethical and Auditing Framework

In the agentic era, trust is not a feature; it is the foundation. As discussed in the "Know Your Agent" (KYA) and liability sections, you cannot afford for ethics and auditing to be an afterthought. This framework must be built into the DNA of your agentic systems from day one.

This means engineering systems for:

- Radical Transparency: Every action and decision made by an agent must be logged in an immutable, easily auditable record. Why was this trade executed? Why was this claim denied? The answer must be instantly accessible.

- Explainability (XAI): Beyond knowing what an agent did, you must be able to understand why. Investing in Explainable AI techniques is crucial for debugging, regulatory reporting, and building trust with both internal stakeholders and customers.

- Continuous Bias Monitoring: Deploy automated systems that constantly test agent decisions for statistical bias related to demographics, geography, or other protected characteristics, ensuring fairness and preventing reputational damage.

By embedding this framework from the outset, you not only mitigate risk but also build a powerful competitive differentiator in an age where digital trust is the ultimate currency.

Conclusion

Key Takeaways:

- The shift from Generative to Agentic AI by 2026 is not an incremental change but a fundamental paradigm shift for the BFSI sector, moving from AI assisted work to autonomous execution.

- While the economic upside is immense measured in trillions of dollars of productivity and rapid ROI the strategic challenges related to systemic risk, compliance (KYA), and liability are profound and require immediate C suite attention.

- The winners in this new era will be the institutions that move decisively to build robust governance, modernize their technology stack, and strategically cultivate a workforce prepared to collaborate with and manage autonomous agents.

Begin developing your organization's Agentic AI strategic roadmap today. Assess your technological readiness, establish a governance framework, and identify the first high impact, contained use case to pilot your journey into the autonomous future of finance.

Published: January 14, 2026

Related Topics

Related Resources

Build AI Agents from Scratch with Python and Gemini: A Beginner Friendly Guide to Use Cases and Challenges

AI agents are moving beyond simple chatbots, and with Python and Gemini, beginners can now start building useful autonomous workflows faster than ever. This article introduces AI agents in a practical, beginner friendly way and shows how Python and Gemini can be used to create them from scratch. It covers the core building blocks, a simple development path, real world use cases, and the main challenges to watch for when getting started.

articleThe Ultimate AI Learning Roadmap for Software Engineers (2025 Edition)

The line between 'software engineer' and 'AI engineer' is disappearing. Are you prepared for the shift from deterministic coding to orchestrating intelligent, probabilistic systems? This comprehensive AI learning roadmap is designed specifically for software professionals. It's a practical, timeline based guide to not only learn the necessary skills but also leverage your existing engineering expertise to transition into a high impact AI role, covering everything from mathematical foundations to production grade MLOps and Generative AI.

videoAI Agents: The Rise of "Smart Digital Workers" (Full Guide)

Are AI Agents just hype, or are they the future of work? Discover the shift from traditional software to AI Agents—"Smart Digital Workers" that use LLMs as a reasoning backbone to think, decide, and act autonomously.